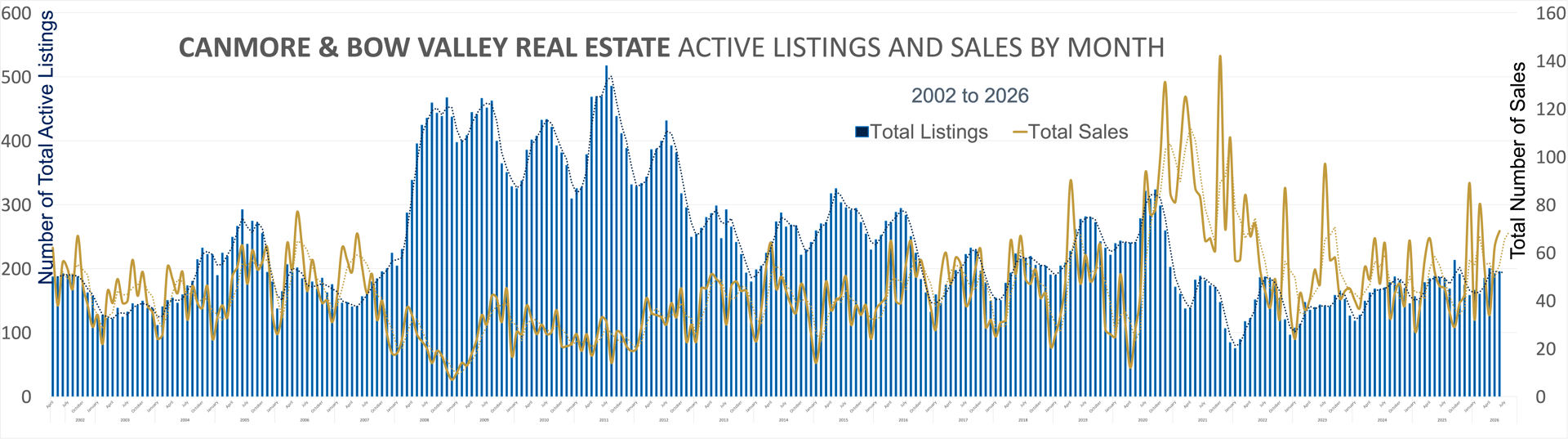

A Fickle Market: Strong Headlines, Softer Foundations

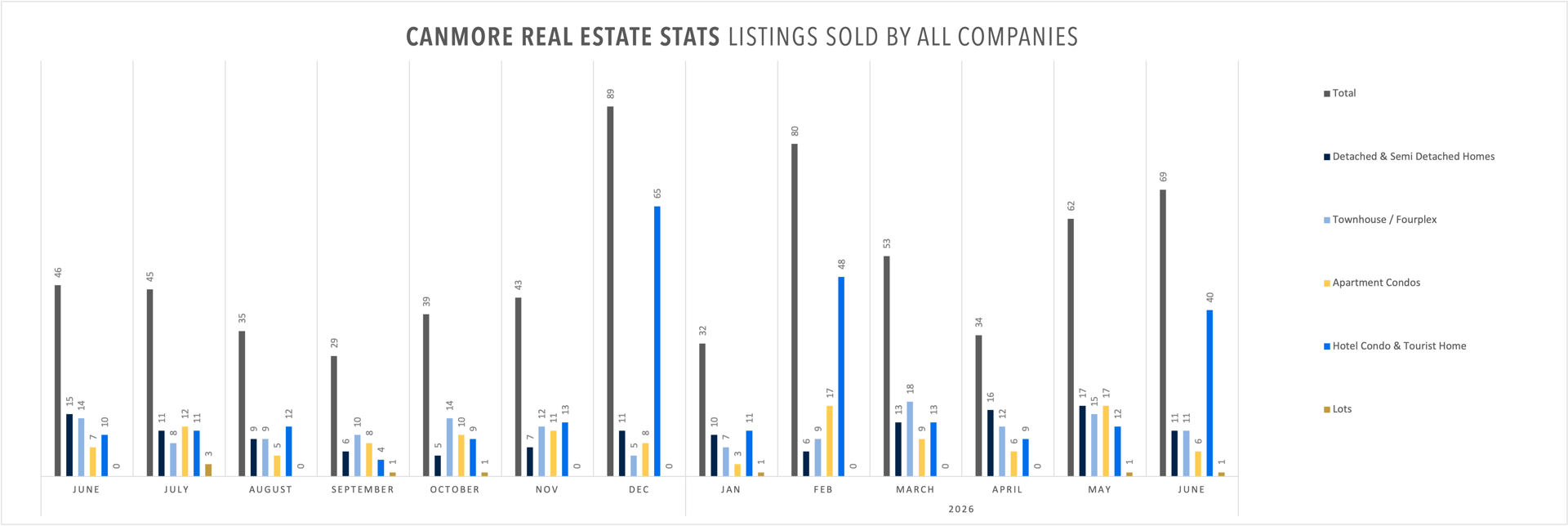

June produced 69 sales — a strong month, but not actually 2026's strongest. That distinction belongs to February, which posted 80 sales on the back of a different new short-term rental building release. Between them, two separate STR project launches — February and June — account for Canmore's two busiest months of the year, while the underlying residential market has stayed comparatively quiet. Look past the headline totals, and demand for detached homes, townhomes, and apartment condos is, if anything, a touch softer than it was a year ago.

This is a market that rewards close attention to segment and product type, not just the headline number.

Sales Activity: February, Then June — Same Pattern Twice

June's 69 sales capped a busy second quarter, with 165 total transactions between April and June — essentially flat compared to the 164 sales recorded over the same three months in 2025.

But June wasn't even the year's high point. February posted 80 sales, and 48 of those came from a different new short-term rental building release. June's total is really a repeat of that same pattern, not a new peak: short-term rentals accounted for 40 of June's 69 sales, and 30 of those came from the new Dead Man's Flats project. Strip STR-driven new-construction activity out of both months, and 2026's sales pattern for detached homes, townhomes, and apartment condos looks steadier — and considerably less dramatic — than either headline total suggests.

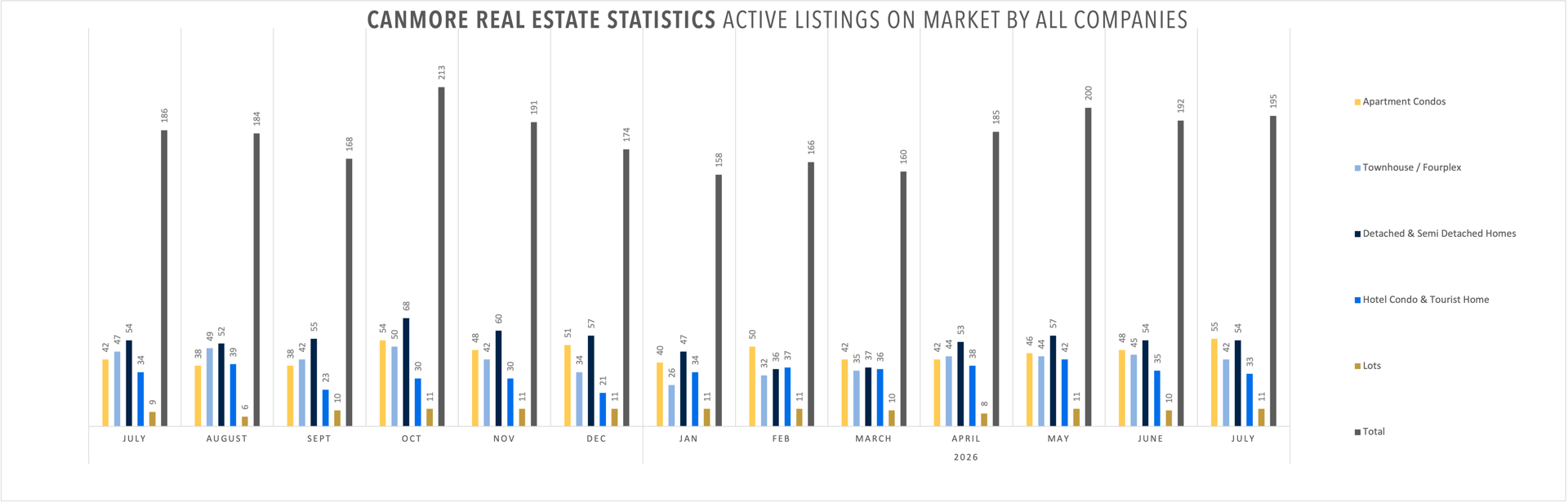

Active listings held close to steady at 192 in June, down slightly from 200 in May and just above April's 185.

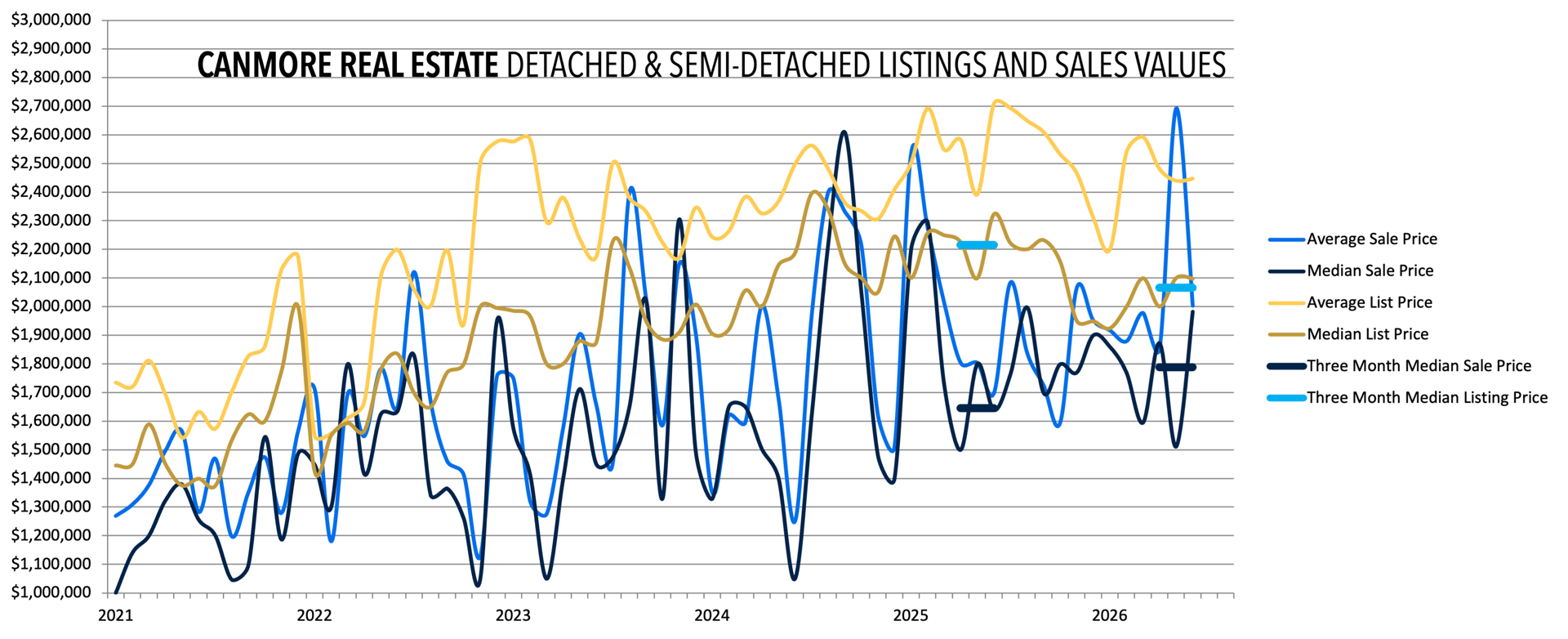

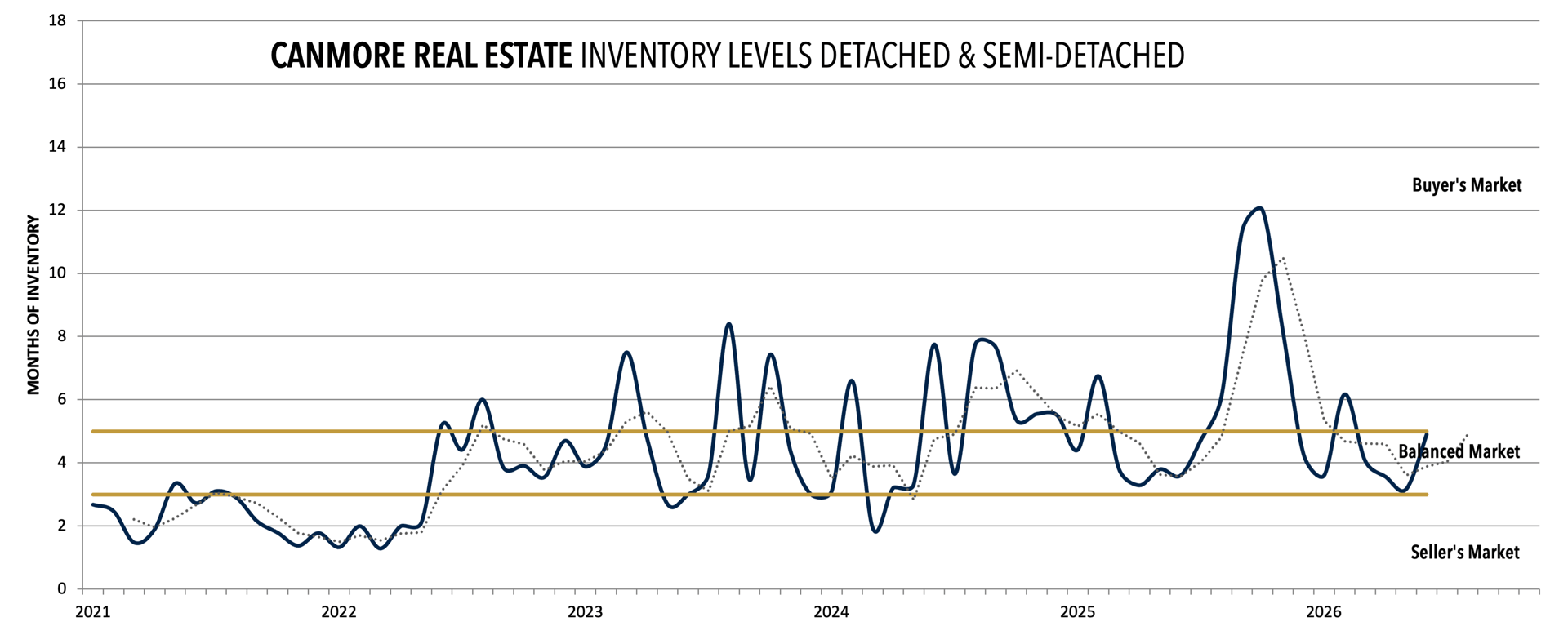

Detached & Semi-Detached Homes: Balanced, With Noisy Pricing

Eleven detached and semi-detached homes sold in June, against 54 active listings — a months-of-inventory reading of roughly 4.9, moving toward the upper end of the balanced range after sitting closer to 3.3–3.4 in April and May.

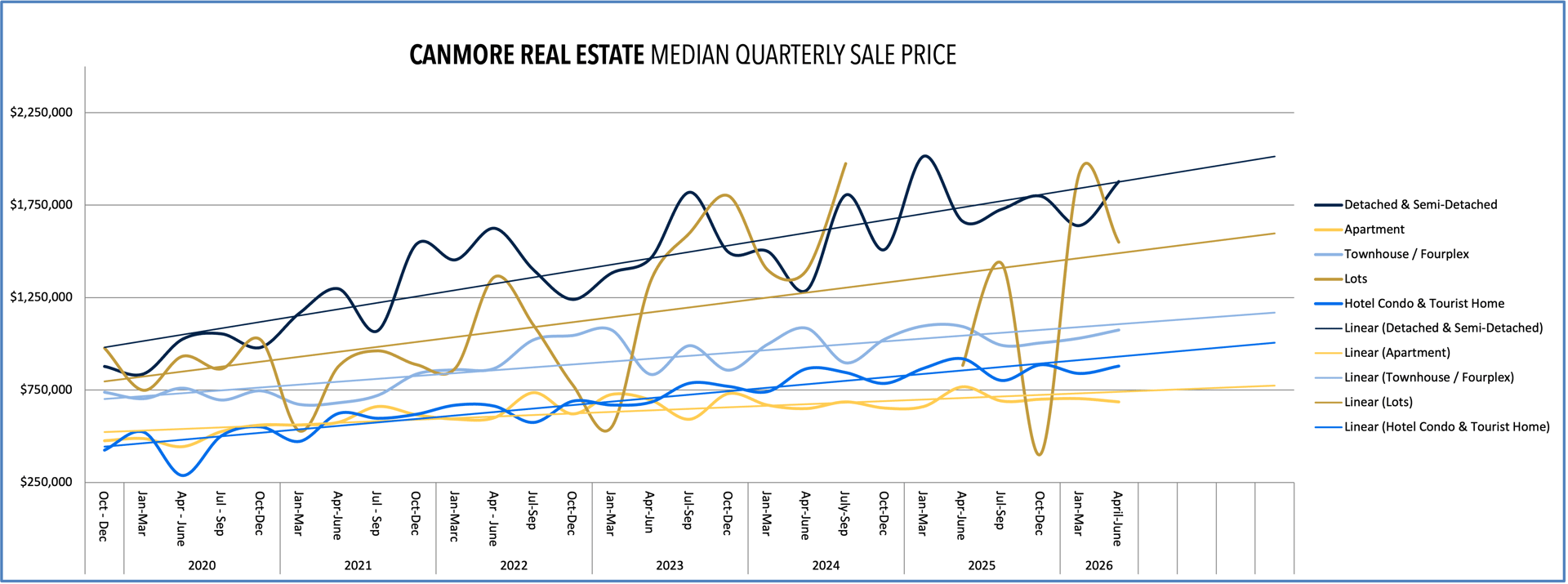

Pricing swung widely month to month: the median sale price moved from $1.87 million in April to $1.51 million in May and back up to $1.98 million in June, with the average sale price spiking to $2.69 million in May on the back of a luxury transaction. At this segment's sales volume — a handful of transactions per month — one or two high-end sales can swing the average considerably, so month-to-month price moves here are better read as noise than trend. On a quarterly basis, Q2 2026 detached sales (44) came in slightly below Q2 2025 (47).

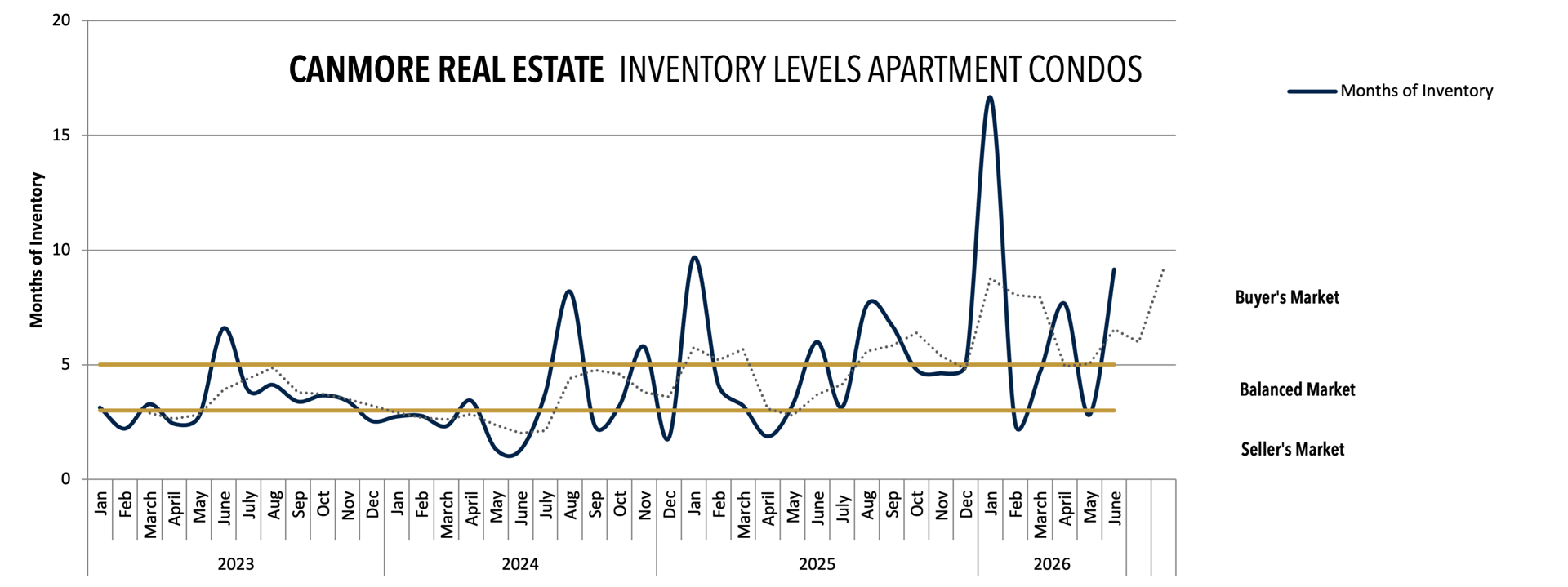

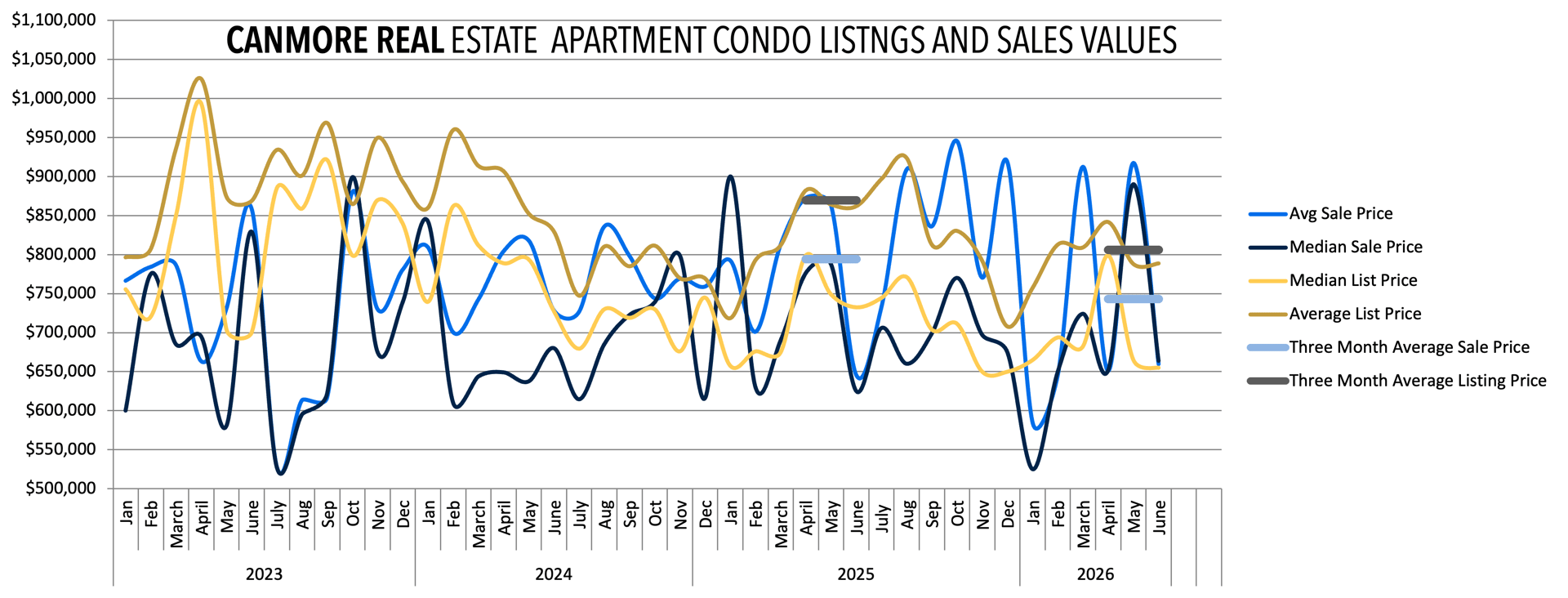

Apartment Condos: The May Numbers Were the Anomaly

Apartment condos are where "fickle" fits best. Inventory sat at roughly 7.0 months in April — already in buyer's-market territory — before dropping sharply to 2.7 months in May, then rebounding to 8.0 months in June.

That May dip wasn't a sudden tightening of the resale market — it was the launch of the sales centre and completion of the first building at Altitude at Three Sisters, which drove 17 condo sales in a single month, more than double April's 6 and June's 6. Once that one-time wave of new-construction activity passed, inventory reverted to the elevated, buyer-favorable levels that have characterized the segment for most of 2026.

Pricing tells a similar story: the median sale price ran from $652,000 in April to $890,000 in May (skewed higher by new-construction product) back down to $664,000 in June — close to where it started. For buyers shopping resale condos, June's numbers are the more representative read: ample selection, patient pricing, and real room to negotiate. On a quarterly basis, Q2 2026 apartment sales (29) trailed Q2 2025 (36).

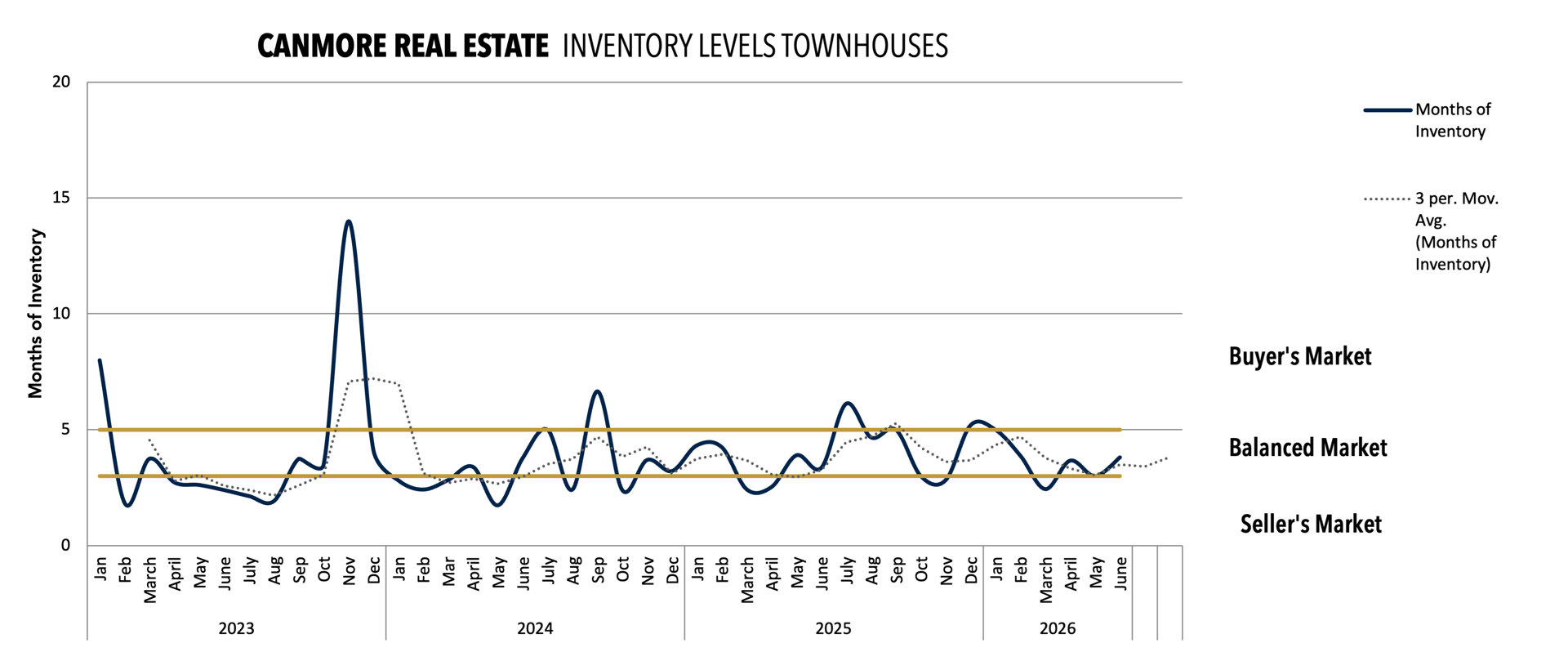

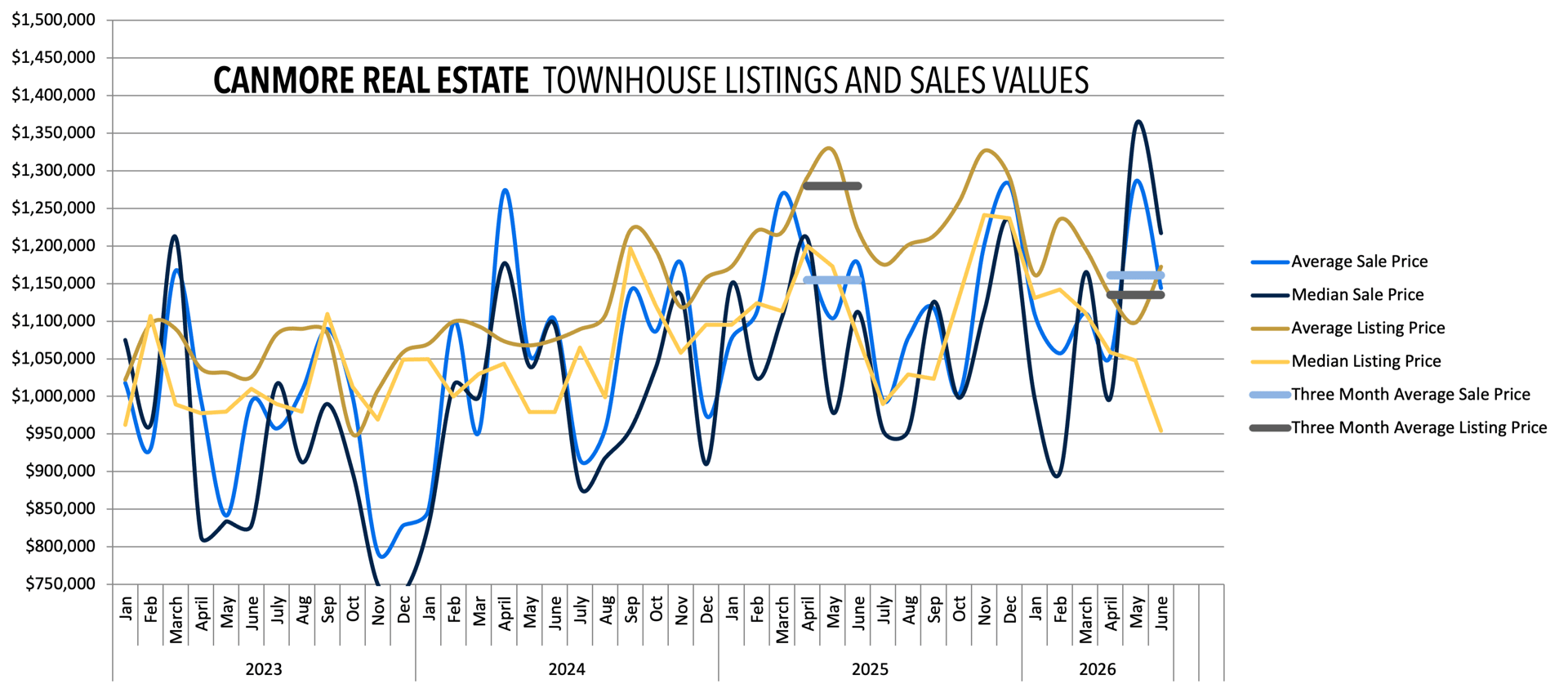

Townhomes: Cooling From a May Peak, Still Firm

Townhomes remain the market's most consistent segment. Inventory moved from 3.7 months in April to 2.9 in May and back to 4.1 in June — balanced throughout.

Pricing peaked in May, with the median sale price reaching $1.36 million, then eased to $1.217 million in June — still well above April's $998,500 and among the stronger months on record for the segment, even after cooling from its spring high. Eleven townhomes sold in June on 45 active listings. Quarterly sales (38 in Q2 2026) came in modestly below Q2 2025's 42, consistent with the broader resale slowdown showing up across property types.

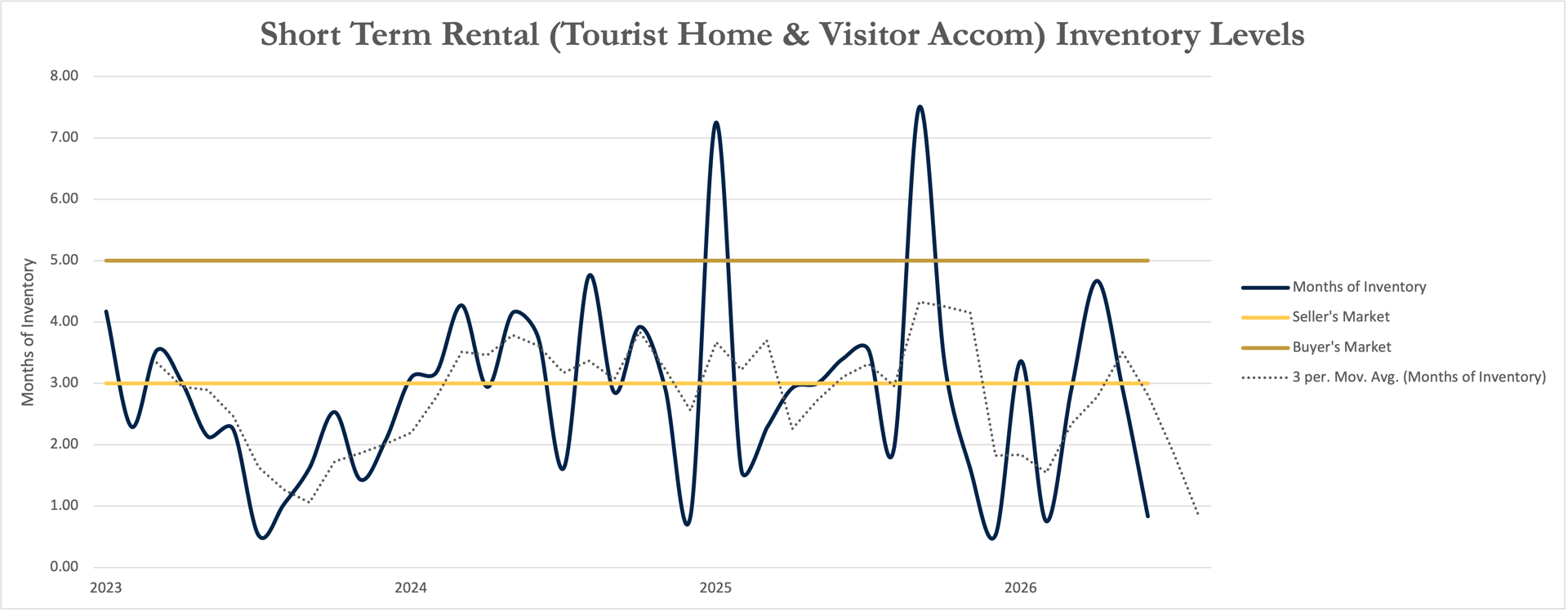

Short-Term Rentals: The Second Big Release of the Year

This isn't the first time a single project has driven a month's numbers in 2026 — it's the second. February's 80-sale month, the actual high point of the year so far, was built the same way, with 48 STR sales tied to a different new building release. June's spike follows the identical pattern: 30 of its 40 STR sales came from the new Dead Man's Flats project.

Total STR sales jumped to 40 units in June from 12 in May and 9 in April, while active listings fell from 42 to 35 as that new inventory was absorbed. Months of inventory collapsed to roughly 0.9 — a level that puts the segment firmly, and unusually, into seller's-market territory.

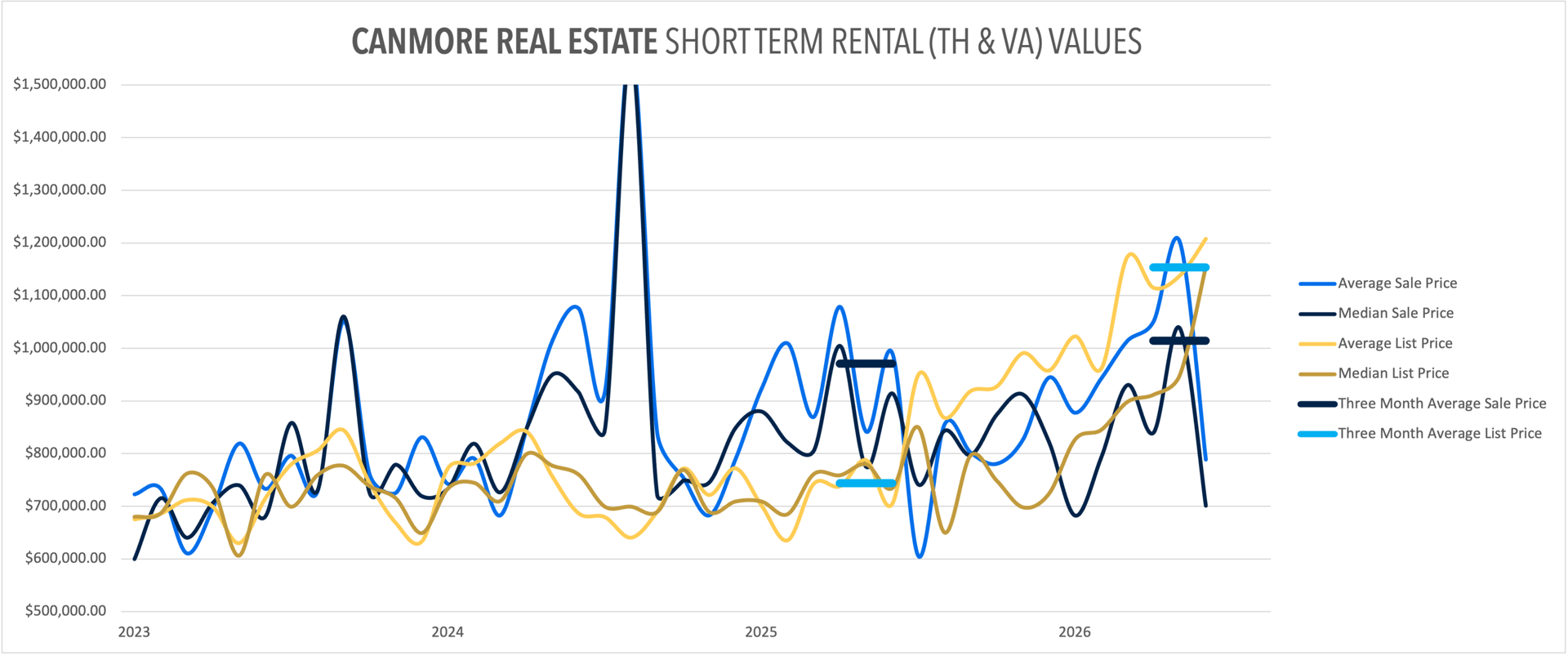

Notably, pricing moved the opposite direction of volume: the median sale price fell to $701,000 in June from $1.04 million in May and $840,000 in April, and the average sale price dropped to $789,000 from $1.2 million. That's consistent with the Dead Man's Flats units being priced to move, layered on top of a still-active organic resale market for the segment's other 10 June sales.

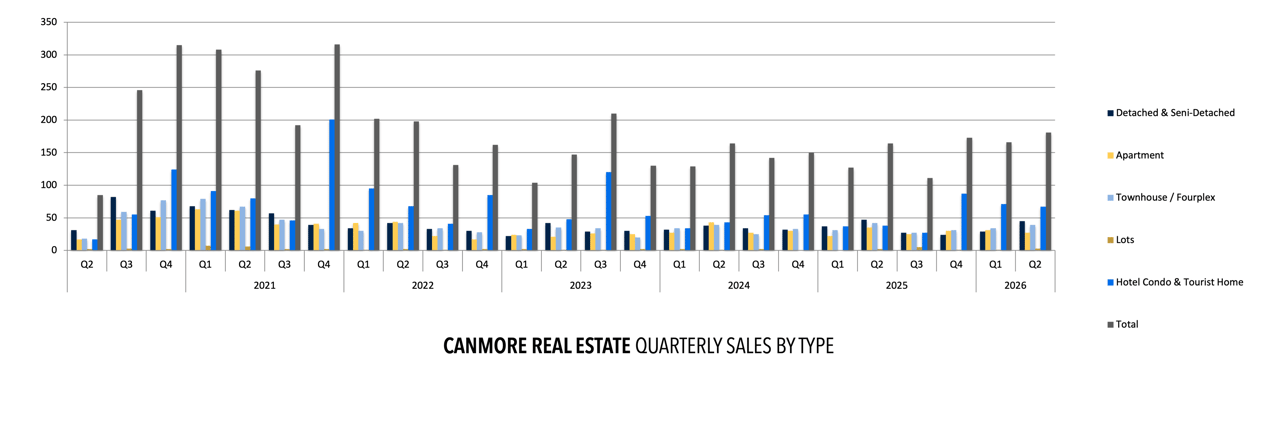

Quarterly, the effect is significant: STR sales totaled 61 in Q2 2026 versus 37 in Q2 2025, an increase of roughly 65%. Add February's 48-sale spike, and Q1 2026 STR volume very nearly doubled year over year (72 vs. 36) — two separate new-construction releases, six months apart, each producing the same short-lived surge.

The Quarterly Picture: Residential vs. Short-Term Rentals

The clearest way to read this year's numbers is to split them the way we track them internally: Residential (detached & semi-detached, townhomes, and apartment condos, grouped together) versus Short-Term Rentals, with Lots set aside since sales volume there is too small a sample to read as a trend.

Residential — Q2 2026 vs. Q2 2025:

- Detached & Semi-Detached: 44 vs. 47 — down modestly

- Apartment Condos: 29 vs. 36 — down about 19%

- Townhomes: 38 vs. 42 — down modestly

- Residential Total: 111 vs. 125 — down roughly 11%

Short-Term Rentals — Q2 2026 vs. Q2 2025:

- 61 vs. 37 — up roughly 65%, with the June Dead Man's Flats release (30 sales) accounting for about half of the quarter's total STR volume

Combined Total: 165 vs. 164 — essentially flat

Every residential category posted fewer sales this quarter than the same quarter a year ago. The only reason total volume held flat is that short-term rental sales — concentrated in one new-construction release — more than made up the difference. Zoom out to Q1 2026 and the pattern holds a similar shape: total sales were up sharply year over year (165 vs. 122), but STR sales alone nearly doubled (72 vs. 36), doing much of the heavy lifting while Residential sales moved only modestly.

None of this means the residential market is weak — detached, townhome, and condo pricing all remain firm to strong. But it does mean 2026's headline sales growth has been substantially a new-construction, STR-driven story, not a broad-based increase in organic residential demand.

What It Means for Buyers and Sellers

For buyers, the read depends entirely on what you're shopping for. Apartment condo buyers have genuine leverage right now — June's inventory levels are among the loosest of the year. Short-term rental buyers are working with an unusually thin, fast-moving pool, largely because one project absorbed most of the available supply. Detached and townhome buyers are operating in a balanced, steady market where preparation matters more than urgency.

For sellers, residential demand has softened slightly compared to a year ago, even as pricing holds firm. That combination — steady prices, quieter transaction volume — puts a premium on accurate pricing and strong presentation to stand out against both residential competition and the pull of new-construction/STR product.

June 2026 Market Snapshot

- Active Listings (All Types): 192

- Total Sales: 69

- Detached & Semi-Detached Inventory: ~4.9 Months (Balanced, Trending Higher)

- Apartment Condominium Inventory: ~8.0 Months (Buyer's Market)

- Townhouse Inventory: ~4.1 Months (Balanced)

- Short-Term Rental Inventory: ~0.9 Months (Seller's Market — New Project Driven)

- Q2 2026 Total Sales vs. Q2 2025: 165 vs. 164 (Flat)

- Q2 2026 Residential Sales (Detached + Townhouse + Apartment) vs. Q2 2025: 111 vs. 125 (Down ~11%)

- Q2 2026 Short-Term Rental Sales vs. Q2 2025: 61 vs. 37 (Up ~65%, ~30 tied to the Dead Man's Flats release)

- Overall Market Condition: Uneven — New Construction/STR Driving Volume, Residential Demand Softer Than a Year Ago

If you are considering buying or selling real estate in Canmore, Banff, Harvie Heights, Dead Man's Flats, Exshaw, or Lac des Arcs, understanding which of these currents applies to your specific property is critical this summer. Working with a local Canmore Realtor who tracks these trends month to month — and knows which numbers are signal versus noise — can help you time your move and price it right.